An apartment community is not a building with units. It is a business in motion, and on closing day that business changes hands mid-stride: hundreds of leases, deposits, options, and possession rights transfer with the deed, along with every recorded covenant, easement, and restriction that decides what the community can charge and what it can become. This is my guide to what multifamily buyers run into across Virginia and West Virginia, and what a careful closing does about each item.

Written by Anthony I. Shin, Esq., Principal and real estate attorney at Prime Title & Escrow

The question is not whether you can buy the community. It is whether the leases, the deposits, the recorded restrictions, the debt, and the title support the income you are underwriting.

About 35 percent of United States households rent their home, and the renter share climbed after 2008 and never returned to its old level, which is why capital keeps moving into apartments. But the income you are buying rides on paper: every tenancy survives the closing, both states bind you to return deposits you may never have received, and recorded affordability covenants can control rents for decades after the original program ends.

This guide walks through the tenant estate, deposits, estoppels, affordability restrictions, shared amenities, zoning, liens, debt, entities, and the closing itself in Virginia and West Virginia, and how my team clears each one. Every figure is attributed to its source, with the full list at the end. This is general educational information, not legal, tax, lending, or regulatory advice for any specific transaction.

I wrote this because multifamily is where a real estate closing most resembles a company acquisition. The asset produces income the day before you own it and the day after, and everything that keeps that income flowing, the tenancies, the deposits, the amenities, the debt, and the restrictions, has to move through the closing intact. My lane is the record, the escrow, and the closing, and I run that lane end to end. Unit inspections, lease audits, market underwriting, and property condition belong to your consultants, managers, and counsel, and I coordinate with them rather than stand in for them. Where the record does not answer a question, I say so, and I point it to the right professional.

You are buying a business in motion, not a building

Tour an apartment community and you see buildings, parking, a pool, a leasing office, and people living their lives. What you do not see is the paper that makes the income real: several hundred rental agreements in force at this hour, a deposit ledger the law will hold you to, an estoppel package your lender will demand, recorded covenants that may cap the rents, easements that carry the driveway and the amenities, and a deed of trust that has to release in the same breath the deed records. The units are the hardware. The paper is the business, and the business is what you are actually buying.

So my thesis for every multifamily buyer is the same one I bring to a data center acquisition or an industrial deal: read the record before you rely on the walk-through. The buyer who reconciles the rent roll, the deposit ledger, the recorded restrictions, and the survey at the letter of intent knows what the income actually rests on. The buyer who waits inherits whatever the record and the statutes say on closing day, and in this asset class the statutes have opinions. That discipline is built into my multifamily acquisition service, and this guide is the long-form version of it.

The market you are buying into

Apartments sit on the most durable demand base in American real estate. United States Census Bureau housing data puts the renter share of households at about 35 percent, and the long arc matters more than the point estimate: the share ran near 31 percent in 2004, climbed through the foreclosure years to roughly 37 percent by 2016, and has settled around 35 percent since, never returning to its pre-2008 level. Roughly one household in three pays rent every month, and multifamily is where most of that demand lives.

That demand is why apartments trade at scale, and scale is exactly what makes the closing itself a risk. The American Land Title Association reports that nearly 60 percent of transactions need three to five title issues resolved before closing, and on a community with hundreds of tenancies, one lender, and several layers of entities, every one of those issues has more places to hide. The demand picture gets your investment committee to yes. The rest of this guide is about making sure the record supports the yes.

The tenant estate: every lease rides through the closing

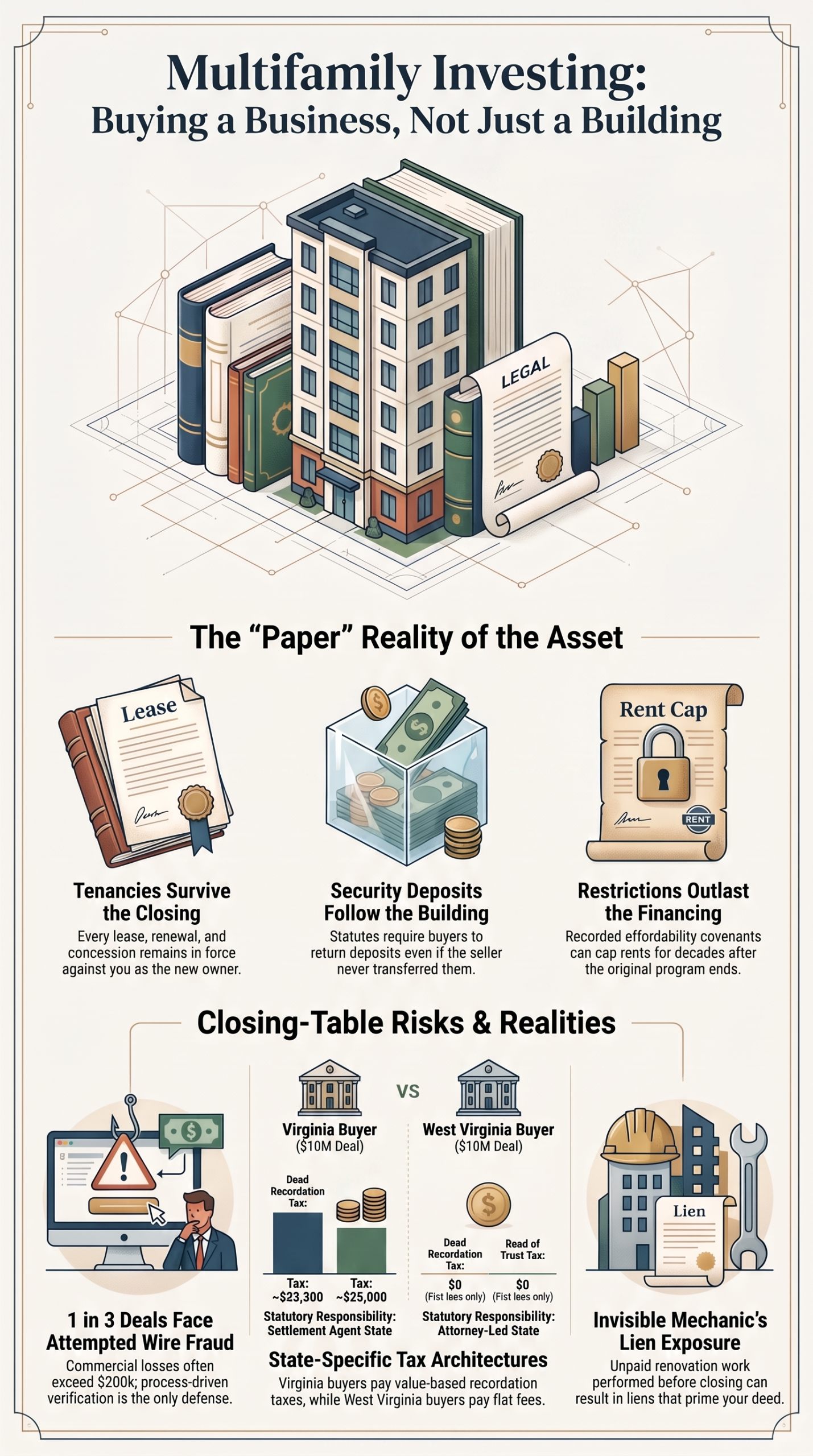

The defining fact of a multifamily closing is that the tenancies survive it. Every lease, renewal, month-to-month holdover, option, concession, and possession right in force at closing continues against you as the new owner, whether or not it appears in the land records, and whether or not the seller’s rent roll mentioned it. You are not buying vacant possession of anything. You are stepping into several hundred existing legal relationships at once, on their existing terms.

Most residential leases are short enough that they never hit the record, so the rent roll, the lease files, and the estoppel process carry the weight a title search carries elsewhere. But the record still matters at the edges: recorded memoranda of lease, recorded options or rights of first refusal from an earlier capital partner, and regulatory agreements recorded by housing programs all bind the property in ways the lease files may not reveal. A right of first refusal recorded a decade ago can complicate your contract today, and it will not be in the leasing office’s filing cabinet.

The practical risk is the gap between the rent roll you priced and the tenancies that exist. Side agreements, rent concessions granted by a prior manager, corporate leases, and units held off-line all change the income without changing the brochure. How we help: I review the recorded layer, memoranda, options, regulatory agreements, and anything else filed against the land, reconcile it against the contract’s rent roll representations, and coordinate with your counsel so the purchase agreement allocates the gap before it becomes your problem.

Security deposits follow the building, not the seller

Here is the statute most multifamily buyers have never read, and it is nearly identical in both states. Under the Virginia Residential Landlord and Tenant Act, Virginia Code Section 55.1-1226, the holder of the landlord’s interest at the time a tenancy ends, regardless of how that interest was acquired, must return any security deposit the original landlord received, whether or not the deposit was ever actually transferred to the new owner, and regardless of any contract between the seller and the buyer. West Virginia Code Section 37-6A-2 says the same thing in almost the same words. Translation: if the seller collected the deposits and spent them, you still owe the tenants, and your indemnity claim against a dissolved selling entity is worth what dissolved entities are usually worth.

The statutes have teeth on the back end too. Virginia caps residential deposits at two months’ rent and puts the return and itemization on a 45 day clock after each tenancy ends. West Virginia runs its own statutory notice periods, and willful noncompliance there entitles the tenant to the deposit plus damages of one and a half times the amount wrongfully withheld under Section 37-6A-5. Multiply any of that across a few hundred units and the deposit ledger stops being a bookkeeping detail and becomes a real liability line.

How we help: I treat the deposit ledger as a closing document. We put the full ledger on the settlement statement, credit the deposits to you at the table rather than trusting a post-closing transfer, reconcile prepaid rent and concessions the same way, and coordinate the tenant notices that tell residents who holds their money now. The day after closing, your obligation exists by statute. The credit that funds it should exist on the closing statement.

Estoppels and SNDAs across a full rent roll

An estoppel certificate is a tenant’s signed confirmation of the basic facts of their tenancy: the rent, the term, the deposit, and whether either side is in default. On an office building with six tenants, collecting them is a task. On an apartment community with four hundred units, it is a project with a deadline, and the deadline belongs to your lender. Agency and bank lenders set estoppel thresholds and forms, subordination and non-disturbance agreements ride alongside them where required, and funding waits on the package.

The trap is sequencing. Estoppels circulated late come back late, and estoppels that come back with surprises, a disputed balance, an unrecorded concession, a deposit the ledger missed, come back at the worst possible moment. Every surprise an estoppel surfaces in closing week was sitting in the file a month earlier, cheaper to resolve.

How we help: we build the estoppel and SNDA tracking list at the front of the file, coordinate with the manager actually collecting signatures, reconcile what comes back against the rent roll and the deposit ledger, and confirm delivery through the escrow before funding. Your lender sees a complete package instead of a promise, and the surprises surface while they are still negotiable.

Affordability covenants that outlast the program

Communities built or renovated with public financing usually carry recorded strings, and the strings outlast the financing. The clearest example is the federal low-income housing tax credit: Internal Revenue Code Section 42 requires an extended use agreement, recorded against the land as a restrictive covenant, that keeps income and rent restrictions in place for at least 30 years in the standard structure. State housing agencies, local programs, and older federal programs record their own versions: land use restriction agreements, regulatory agreements, and deed covenants that cap rents, restrict who may live in the units, limit transfers, and sometimes give an agency approval rights over your purchase itself.

None of that makes a property unbuyable. Restricted communities trade every week, and for the right buyer the restrictions are the strategy. What makes them dangerous is discovering them after you have underwritten market rents. A covenant recorded in 1998 does not care what your pro forma assumed in 2026, and it binds you the moment the deed records, exactly like the recorded conditions I flag for data center buyers whose sites carry old proffers.

How we help: I surface every recorded restriction, covenant, and regulatory agreement in the chain, read it against the income you are underwriting, flag transfer-approval and notice requirements that add parties to your closing, and coordinate with your counsel and lender on what each instrument means for the deal. The restriction is rarely the problem. The surprise is.

Access, parking, pools, and the shared-amenity record

Apartment communities share more than most buyers expect. Phased developments split across parcels, and the driveway, the clubhouse, the pool, the parking ratios, the stormwater pond, and the utility lines often serve the whole community through recorded cross-easements and declarations rather than sitting neatly inside your boundary. A community can also lean the other way, granting rights to neighbors: a shared entrance with the retail parcel out front, drainage from the subdivision behind, an access easement that predates the buildings.

The failure mode is buying the buildings and missing the glue. If the pool sits on a parcel the deed does not convey, if the second entrance runs on a neighbor’s land without a recorded right, or if the declaration that governs the shared amenities carries assessment obligations nobody modeled, the community you toured and the property you bought are not the same thing. Parking deserves its own line: zoning approvals and lending both assume the ratios, and ratios that depend on an unrecorded arrangement with the parcel next door are ratios you do not actually have.

How we help: I verify every recorded access, parking, amenity, utility, and drainage right against the ALTA survey, parcel by parcel, confirm which parcels give and which receive each benefit, surface the declarations and their cost-sharing terms, and flag the gaps while they are still contract issues. The survey and the record have to tell the same story before your capital sits at the table.

Zoning, proffers, and the nonconforming community

A large share of the apartment stock in both states was built under zoning that no longer exists. Districts changed, parking standards changed, density rules changed, and the community kept operating as a legal nonconforming use. That status is usually stable, but it is also brittle: casualty, expansion, and redevelopment can each test whether the grandfathering survives, and the answer decides whether you can rebuild what you bought. If your underwriting includes adding units, a fourth phase, or a substantial reconfiguration, the entitlement question belongs at the letter of intent, not after.

The record carries its own zoning layer. Communities that came through a rezoning often carry recorded proffers and conditions, commitments the original developer made decades ago that run with the land: a road improvement, a buffer, a recreation requirement, a cap on units. Those bind you regardless of what the seller remembers, and they interact with everything else in this guide, from the parking ratios to the amenity parcels.

How we help: my lane is the recorded layer. I surface the proffers, conditions, and covenants filed against the land and put them in front of you and your land use counsel with dates and instruments attached. Zoning strategy, nonconforming-use analysis, and entitlement work belong to that counsel, and the record I deliver is the foundation they build on.

Renovation work and invisible lien exposure

Value-add is the dominant multifamily strategy, which means the property you are buying has probably seen recent contractor work: unit turns, roofs, amenity upgrades, a rebranding. In Virginia, that history matters at closing because a mechanic’s lien under Title 43 relates back to when the work began, not when the claim is filed. A contractor unpaid for work performed before closing can perfect a lien after closing, with a priority date that steps in front of your deed. West Virginia’s lien framework under Chapter 38, Article 2 of its code carries the same essential threat. A clean title search on closing day is a starting point, not a verdict, and the mechanics are the same ones I walk through for industrial construction liens.

How we help: we ask the questions the search cannot answer. What work was performed in the lien window, who performed it, and who has been paid. We collect lien waivers and contractor affidavits through the escrow, and where real exposure remains, we hold funds in escrow until the window closes or the releases arrive. On a value-add deal, the renovation history is a title document, and we treat it like one.

Payoff, assumption, or consent: three paths for the existing loan

Almost every multifamily community carries debt, and the existing loan takes one of three paths through your closing. It can be paid off and released, which requires exact payoff figures, per diem interest, and a release the record will actually reflect. It can be assumed, common with agency debt, which puts you through the lender’s approval process on the lender’s timeline, with fees, reserves, and documentation of its own. Or the transaction can require the lender’s consent for a structure change even where the debt stays in place. Each path has a different clock, and the clock starts when the path is chosen, so choosing late is its own risk.

Prepayment economics belong in the model early. Agency and institutional loans commonly carry yield maintenance or defeasance provisions, and the cost of exiting the debt can move the deal math as much as the price. That analysis belongs to you and your debt advisors; what belongs to me is making sure the chosen path lands at the table. How we help: we obtain payoff and release requirements in writing, or run the assumption and consent checklist alongside the lender, track every deliverable to the closing date, and sequence the funding so the release, the deed, and the new deed of trust record in the right order. The loan is the largest lien on the property, and it deserves the most disciplined file.

Entities, funds, exchanges, and foreign sellers

Multifamily buyers rarely take title in their own names. The buyer is a single-purpose entity under a fund, a joint venture with an operating partner, tenants in common completing an exchange, or an out-of-state platform entering the market. Every layer adds a document the closing needs: formation records, resolutions, consents, and a signature block that actually binds the entity signing. Authority defects are the quietest way to lose a closing date, because nobody looks for them until the documents are in front of a notary.

Two federal layers deserve a line. If you are closing a 1031 exchange, the identification and closing deadlines are absolute, and the escrow has to be built around them from day one. And if any seller in the chain is a foreign person, federal law generally requires withholding a portion of the price at closing under the Foreign Investment in Real Property Tax Act, which is a settlement-table obligation with real liability attached. How we help: we collect and verify entity and authority documents at the contract stage rather than closing week, coordinate exchange mechanics with your intermediary, screen for withholding obligations, and match every signature block to the structure chart before signing day.

Virginia and West Virginia, side by side

The two states agree on more than they differ for multifamily. The tenant estate survives closing in both. The deposit statutes mirror each other almost word for word, binding the new owner either side of the state line. Mechanic’s liens relate back in both. The differences concentrate at the closing table itself, and they are worth knowing before you model your first deal across the border.

Virginia is a settlement-agent state: licensed settlement agents, including attorney-led firms like mine, conduct closings, and the transfer taxes stack the way the next chapter shows, with the buyer carrying the recordation and deed of trust taxes and the seller carrying the grantor’s tax plus regional fees in Northern Virginia. West Virginia treats the closing itself differently: the West Virginia State Bar’s unauthorized practice guidance, Committee Opinion No. 2003-01, treats title examination and the conduct of the closing as the practice of law, so a licensed West Virginia attorney belongs on the closing team from the first week. West Virginia’s transfer excise under Code Section 11-22-2 falls on the seller by default, and the state imposes no value-based tax on recording your deed or your deed of trust, which quietly favors debt-financed buyers.

How we help: my firm runs attorney-led files as a matter of design, so the West Virginia posture is not an adjustment for us, and on cross-border portfolios we coordinate West Virginia counsel, county-by-county recording requirements, and the different tax math through one open-items list instead of two parallel processes.

The closing: what recording the deed costs

Here is the closing-week math on a $10,000,000 community, sourced line by line. In Virginia, the buyer pays the state recordation tax of $0.25 per $100 under Code Section 58.1-801 plus the local third under 58.1-814, about $33,300 together. A financed buyer also pays the deed of trust recordation tax under 58.1-803, $0.25 per $100 on the first $10,000,000 of debt, which is $25,000 of state tax alone before the local third. The seller pays the grantor’s tax of $0.50 per $500 under 58.1-802, $10,000 on this price, and in the Northern Virginia jurisdictions adds the WMATA Capital Fee under 58.1-802.3 and the Regional Congestion Relief Fee under 58.1-802.4, bringing the seller’s side to $30,000.

In West Virginia the architecture inverts. The transfer excise under West Virginia Code Section 11-22-2 falls on the seller by default and runs from $33,000 at the floor to $55,000 at the maximum county rate on a $10,000,000 conveyance, while the buyer records the deed and the deed of trust for flat fees with no value-based tax at all. Allocation is negotiable in both states, so treat every line as the statutory starting position for the contract rather than the ending one.

Two more lines belong in the model even though they are not taxes. The deposit ledger from chapter four should appear as a credit on the settlement statement, and prorations, rents collected for the month of closing, utility charges, and program payments where they exist, should be reconciled against the actual rent roll rather than an estimate. On a community of any size, sloppy prorations cost more than the recording taxes.

Wire fraud at rent-roll scale

A multifamily closing concentrates every risk factor the wire fraud data warns about: a large purchase wire, a payoff wire, a deposit credit, multiple entities, multiple advisors, and a long email chain connecting them. The Federal Bureau of Investigation’s Internet Crime Complaint Center has tracked tens of billions of dollars in business email compromise losses, and the land title industry’s own numbers put an attempted wire fraud on roughly one in three real estate transactions, with average losses of $150,000 to $200,000 and commercial deals running higher.

The defense is process, applied without exception. Wire instructions are established at the opening of the file and verified by phone with known contacts. No change to payment instructions is ever accepted by email, no matter how urgent the message sounds or whose signature block it carries. Funds disburse only when written closing conditions are met. How we help: those rules are how my escrow runs on every file, and on a purchase this size they are the difference between a closing and a company-altering loss.

Challenges, and how we clear them

Six issues account for most of the friction on multifamily files, and each one has appeared in this guide. Tenant estates and possession: every tenancy survives the closing, so we reconcile the recorded layer against the rent roll and coordinate delivery through the escrow. Deposits: both states bind you by statute, so the ledger goes on the settlement statement as a credit at the table. Estoppels and SNDAs: we build the tracking list early, coordinate the collection, and confirm the package before funding. Affordability and use restrictions: we surface every recorded instrument and read it against the income you underwrote. Shared access, parking, and amenities: we verify each recorded right against the ALTA survey, parcel by parcel. Recent renovation work: we investigate the lien window, collect waivers, and escrow where exposure remains.

None of these is exotic, and nearly all of them are curable when they surface at the letter of intent. The pattern across every one is the same: the record and the statutes decide what you actually bought, and the closing is where the record, the money, and the paperwork either land together or do not. Getting them to land together is the job, and it is the whole reason the file runs through attorneys. The broader framework, if you want it, is on my page explaining what a title and escrow company does, and if you are on the other side of one of these deals, the disposition version lives on my multifamily selling page.

Send me the contract or the letter of intent, the entity documents, and your lender’s contact, and my team will open the file, order the title and survey, and put the tenant estate, the deposits, and the record on one tracked list from day one.

Get Your Free Quoteor call (703) 552-4155This guide pairs with my multifamily title and settlement service and its disposition counterpart for multifamily sellers. The sibling guides cover the other two asset classes in depth:

The data center buyer’s guide to Virginia and West Virginia • The industrial buyer’s guide to Virginia and West Virginia

We close across Virginia and West Virginia, with deep experience in the renter markets where apartment communities trade most often:

Northern Virginia: Fairfax County, Arlington County, Alexandria, and Loudoun County.

Richmond metro: Richmond, Henrico County, and Chesterfield County.

Hampton Roads: Norfolk, Virginia Beach, Newport News, and Hampton.

Questions multifamily buyers ask me

The community is fully occupied. What actually happens to the tenants at closing?

Nothing, and that is the point. Every tenancy continues on its existing terms against you as the new owner, by operation of law, whether or not the lease appears in the land records. What changes hands is the landlord’s side: the deposit obligations transfer to you by statute in both states, rents prorate on the settlement statement, and residents receive notice of who owns the community and who holds their deposits. The work is making sure the rent roll you priced, the deposit ledger you were credited, and the tenancies that exist are the same list.

The property has recorded affordability covenants. Can we still buy it?

Usually yes, and for some buyers the covenants are the strategy. Low-income housing tax credit properties carry extended use agreements recorded as restrictive covenants, at least 30 years in the standard structure under Internal Revenue Code Section 42, and other programs record their own regulatory agreements. What matters is reading every recorded instrument against the income you are underwriting before you commit, and flagging any agency approval or notice rights that add a party to your closing. The restriction rarely kills the deal. The surprise does.

Who pays the recordation and transfer taxes on a multifamily purchase?

In Virginia, the buyer pays the state recordation tax of $0.25 per $100 plus the local third, about $33,300 on a $10,000,000 purchase, and the deed of trust tax on financed deals, while the seller pays the grantor’s tax plus regional fees in Northern Virginia. In West Virginia, the transfer excise falls on the seller by default, $33,000 to $55,000 on the same price depending on the county, and the buyer records the deed and deed of trust with no value-based tax. Every allocation is negotiable by contract, so treat the statutory defaults as the starting position.

Sources

Every figure in this guide is drawn from the sources below, current as of the dates shown. Where a source did not provide a figure, I have left it out rather than estimate.

United States Census Bureau. Housing Vacancies and Homeownership (renter share of households). https://www.census.gov/housing/hvs/index.html

Code of Virginia, § 55.1-1226, Security deposits, Virginia Residential Landlord and Tenant Act. https://law.lis.virginia.gov/vacode/title55.1/chapter12/section55.1-1226/

West Virginia Code, § 37-6A-2 and § 37-6A-5, Residential Rental Security Deposits. https://code.wvlegislature.gov/37-6A-2/

Internal Revenue Code, 26 U.S.C. § 42(h)(6), extended low-income housing commitment. https://www.law.cornell.edu/uscode/text/26/42

Code of Virginia, Title 58.1, Chapter 8, State Recordation Tax, §§ 58.1-801 through 58.1-814. https://law.lis.virginia.gov/vacodefull/title58.1/chapter8/

West Virginia Code, § 11-22-2, Excise tax on privilege of transferring real property. https://code.wvlegislature.gov/11-22-2/

Code of Virginia, Title 43, Mechanics’ and Materialmen’s Liens. https://law.lis.virginia.gov/vacodefull/title43/

West Virginia Code, Chapter 38, Article 2, Mechanics’ liens. https://code.wvlegislature.gov/38-2/

West Virginia State Bar, Committee Opinion No. 2003-01 (unauthorized practice of law; real estate settlement services). https://wvbar.org/wp-content/uploads/2012/04/AO-2003-01.pdf

Internal Revenue Service. Reporting and paying tax on U.S. real property interests (FIRPTA). https://www.irs.gov/individuals/international-taxpayers/reporting-and-paying-tax-on-us-real-property-interests

American Land Title Association, industry data cited in text (risk cleared annually; share of transactions requiring title issue resolution; wire fraud attempt and loss figures, with Stewart). https://www.alta.org/

Federal Bureau of Investigation, Internet Crime Complaint Center. Business email compromise: The $50 billion scam. https://www.ic3.gov/PSA/2023/PSA230609

This guide provides general educational information for Virginia and West Virginia and is not legal, tax, lending, landlord-tenant, housing-program, or regulatory advice for any specific transaction. Every acquisition requires review of its own property, documents, parties, leases, and title-insurance terms. Data and legal frameworks are attributed to third-party sources and reflect the dates those sources describe, and both continue to change. Please confirm anything you intend to rely on, and reach out to me directly with questions about your own acquisition.